Storage costs are not what they used to be. UK warehouse rents have risen steadily through the post-pandemic period, and the standard commercial response (sign a five-year lease and forget about it) does not fit a business whose volume might double or halve inside the same year. For founders running growing startups and small businesses, the question is not whether to use a warehouse. It is which storage model survives the next eighteen months of growth uncertainty.

Why traditional warehouse leasing has stopped working for small businesses

The standard UK industrial lease is a three to five-year commitment on fixed square footage at a fixed annual rent (with the usual upward review clauses). That structure was designed for businesses with predictable, stable volume. It does not match the realistic operating profile of a startup or growth-stage SME, where the volume curve is steep, lumpy and frequently revised.

The mismatch creates two specific problems. First, the cost of being wrong about volume is asymmetric. Over-leasing means a startup carries fixed cost on space it does not use, eating into runway. Under-leasing means scrambling for additional space during peak when the wider market is tight and the rate is least favourable. Second, the long commitment locks the founder out of taking advantage of market shifts. The geography, the product line and the operating model might all change inside the lease term, and the lease cannot.

The market backdrop has made this worse rather than better. UK prime industrial rents have climbed materially since 2021, driven by the structural shift to e-commerce, constrained new supply in the southern corridors and the same competitive demand that pushed up land values. For small businesses, this means the cost of being wrong on a long lease is higher in absolute terms than it would have been a decade ago.

“The first step is actually making the deliveries yourself or having the people come at the door.”

Christopher Chilton, Co-founder of Ram Tang Cello

How tech-enabled storage changes the cost picture

The other half of the story is that storage technology has become substantially more sophisticated even at smaller scales. Five years ago, a small business serious about warehousing had two choices: sign a long lease and run an in-house operation, or hand the lot to a 3PL on a transactional contract. Both options came with substantial overheads that did not fit a startup operating model.

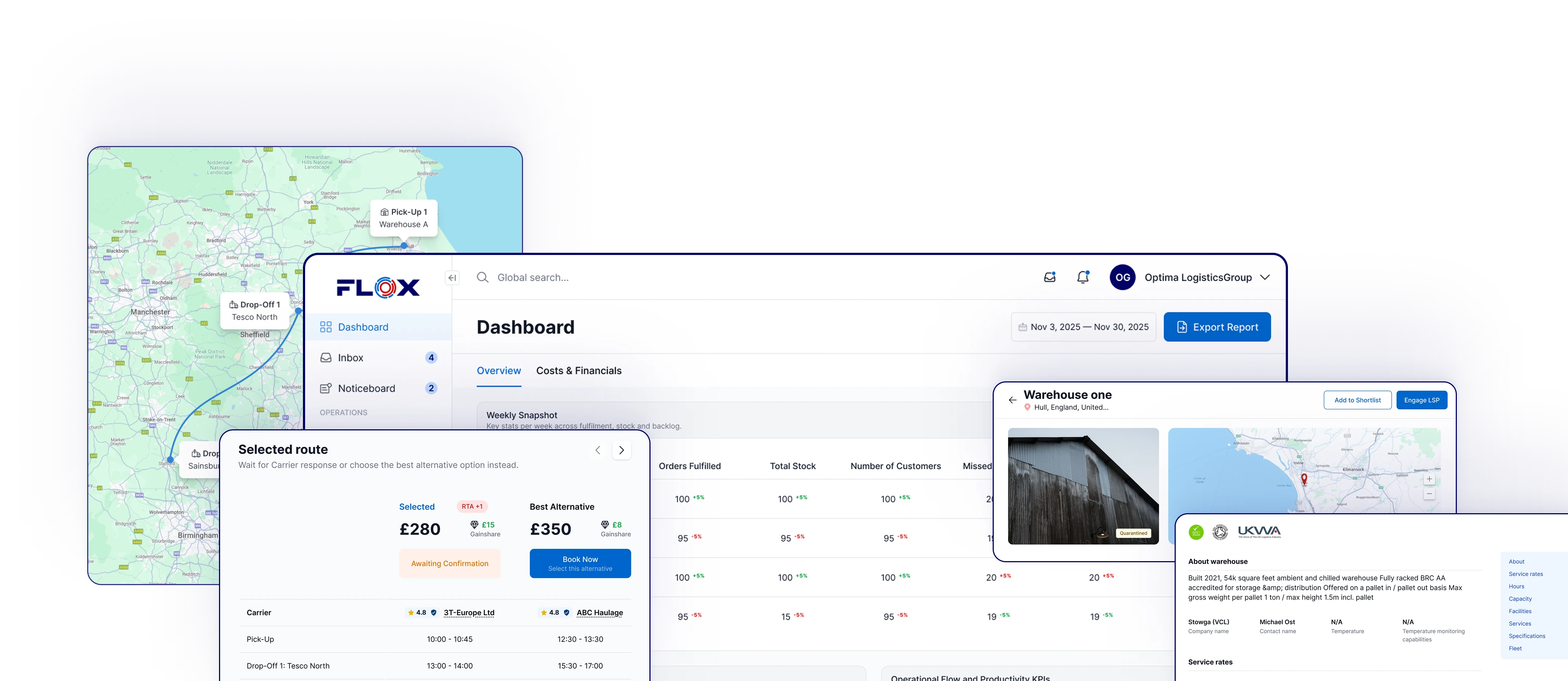

The newer pattern is on-demand or pay-as-you-go warehousing, where storage is priced by pallet, by month, with short notice periods and the option to scale up and down as volume moves. The Warehouse Management System (WMS), the picking, the despatch all happen on the provider side, but the data flows back to the startup in real time. The result is that a founder can see what is in stock, where it sits and at what cost without having to run the operation themselves.

A few capabilities have moved from optional to standard in this segment. Real-time stock visibility through the provider's WMS. Order management that integrates with the buyer's e-commerce platform. Despatch reporting that ties shipments to customer orders. Carrier-rate transparency on outbound shipments so the founder can see the all-in cost-to-serve, not just the storage component. None of these were normal for small accounts five years ago. All of them are accessible now through the right provider relationship. The wider operational case for going this route is set out in our piece on should you invest in your own warehousing or outsource it.

Stephen Holcomb

Director of Logistics at Refeyn

Chain Reaction Podcasts

Choose Partners, Not Just Providers

There's a world of difference between a logistics provider and a logistics partner. Stephen explains what he looks for — and why most companies get the distinction wrong.

What to look for in a flexible storage service

For a founder evaluating storage providers, the technology checklist is necessary but not sufficient. The harder filter is operational. Four questions cut through most of the marketing noise.

First, what is the minimum commitment? A provider offering true on-demand storage will price by pallet or by cubic foot, with monthly billing and a short notice period (typically 30 days). A provider with a three-month minimum term and an annual price is not flexible; they are a traditional 3PL using marketing language. The minimum-commitment answer separates the two cleanly.

Second, how transparent is the all-in cost per shipment? Storage rate is only one cost line. Picking, packing, packaging, returns processing and outbound carrier rates can together amount to more than the storage line itself. Providers that publish their handling rates upfront are easier to budget against than those that quote storage cheaply and recover margin through handling fees.

Third, what does scale-up actually look like? A provider with depth in one site only is fine until the business outgrows that site. A provider with capacity across multiple locations (or running on a marketplace with access to multiple providers) absorbs growth without forcing a migration. The growth-path question is rarely asked early enough.

Fourth, what is the data flow back to the buyer? The right answer is real-time visibility of stock, orders, shipments and exception events, in a format that the founder's own systems can consume. Anything less leaves the founder running parallel spreadsheets, which defeats the operational point of outsourcing.

Common mistakes growing companies make on storage

Patterns repeat. Three mistakes dominate in startups that get to scale and look back at the storage decisions they wish they had made differently.

The first is over-committing too early. A founder signs a long lease at the moment of strongest optimism (typically right after a fundraise or a hot quarter) and ends up carrying the cost when the business model pivots or growth comes slower than the plan assumed. The cure is to default to the most flexible option available at every decision point until the volume profile is genuinely stable.

The second is treating storage as a procurement decision rather than an operational one. Storage providers vary enormously in operational maturity, technology integration and customer service. The cheapest pallet rate often hides operational weakness that costs more downstream in service failures than the provider saves on the storage line. The fix is to evaluate storage providers on the same operational criteria you would evaluate a fulfilment partner, not just on the headline rate. Our piece on finding the perfect UK warehouse location covers the locational side of this decision; the operational side is set out in warehouse best practice: getting the basics right.

The third is under-investing in the integration layer. A storage provider connected by manual email handoffs is cheaper to set up than one connected by API, but the cost of the manual layer accumulates fast. By the time the business is shipping several thousand orders a week, the founder is the integration layer themselves and growth stalls because there is no time to do anything else. Build the API integration into the procurement decision from day one. For the broader rental-mechanics side, our piece on perfect warehouse rental near you walks through what a clean rental relationship looks like in practice.

Explore storage and fulfilment solutions that give your business flexibility and the support it needs to grow.

Why marketplace plus orchestration suits the startup operating model

The two structural problems for startups in storage (long commitments and fragmented data) are solved more cleanly by a marketplace plus orchestration model than by a traditional single-provider relationship. The marketplace layer means the founder is not locked into one supplier and can move some or all of the volume to a different provider as the business needs change. The orchestration layer means the founder gets a single view of stock, orders and shipments regardless of how many providers sit underneath.

This is the operating model FLOX is built around. For an SME, it changes the storage decision in three ways. First, the upfront commitment goes down: the founder can start with one provider on flexible terms and add capacity through the marketplace as volume grows. Second, the data picture is consolidated: stock, orders and shipments flow through the orchestration layer regardless of which provider is handling a given shipment, so the founder does not run separate dashboards. Third, the cost of being wrong about volume falls: capacity flexes through the marketplace rather than being locked in long property contracts.

The honest summary for a growing startup is this. The traditional warehouse lease was designed for a business that does not look much like yours. The on-demand and marketplace-based models are designed for the operating profile you actually have. Use them while the volume is moving, and revisit the conventional question of owned versus leased space once the volume stabilises (if it ever does).

Subscribe to our newsletter.

Stay up to date with practical insights and useful logistics content

FAQs

The post-pandemic shift to e-commerce permanently raised the demand for warehouse space, particularly in the southern corridors and around major UK ports. At the same time, new supply has been constrained by high construction costs, planning complexity and elevated borrowing costs that make developers cautious. The result is a structural imbalance: demand has been steady, supply has not kept up, and prime rents have climbed even as broader economic activity has moderated. For small businesses, this means the cost of being wrong on a long lease is higher than it was a decade ago.