The classic question every supply chain leader gets pushed to answer at some point: keep warehousing in-house or hand it to a specialist. The textbook arguments line up on both sides, but the operating reality has shifted in the last few years. This piece walks through what each side actually means in 2025, where the trade-offs sit now, and how the rise of marketplace plus orchestration platforms is starting to reshape the question itself.

The strategic case for owning warehousing

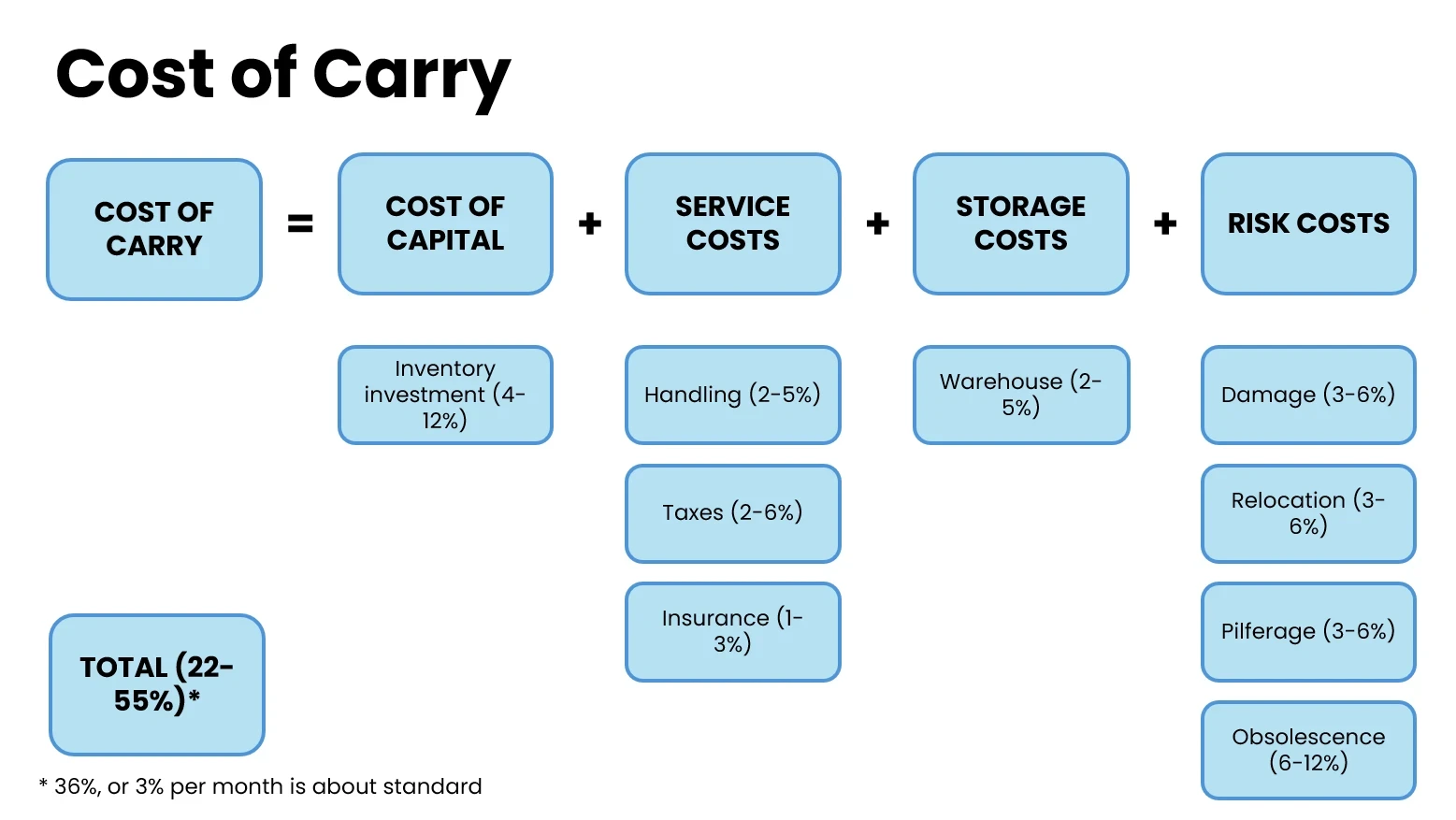

The standard argument for keeping warehousing in-house is that it can be a source of competitive advantage. For some sectors that is genuinely true. In chemicals, building products and some food categories, warehousing costs can run at 4 to 5 percent of revenue. A retailer or manufacturer that can squeeze that line item harder than its competitors creates real margin advantage. Amazon built its consumer-internet dominance on exactly that thesis, and the model worked.

The catch is what the model costs to run at the level Amazon runs it. The company operates a global fleet of large fulfilment centres backed by a multi-billion-dollar technology stack across robotics, software and inventory analytics. Most businesses asking the invest-or-outsource question are not in that bracket. Building warehousing as a competitive weapon requires investment at a scale that is genuinely unusual.

The honest commercial test for owning warehousing is simple. Will the business invest enough to run a top-decile operation, and is warehousing performance directly observable to the end customer in a way that justifies that investment? For an e-commerce category leader the answer is often yes. For most other businesses the answer is no, and the strategic argument for ownership starts to wobble.

“The logistics industry is a unique industry because by default, de facto, it has to collaborate. FLOX is built to enable exactly that.”

Paul Brooks, MD or GFC, Author

What great warehousing actually costs in 2025

The cost picture for warehousing has moved significantly since the late 2010s. Prime warehouse rents have risen across most UK markets through the post-pandemic period, driven by the structural shift to e-commerce and limited new supply in the locations buyers actually want (the M1, M6, M62 and London-area corridors). Land constraints in urban centres push secondary sites into the mix and lengthen the average distance between warehouse and final customer.

Labour and energy costs have moved alongside rent. Wages for picker and packer roles have climbed as the labour market for warehouse staff has tightened, and electricity costs across the UK and Europe sit well above their pre-2022 baseline despite some recent moderation. The combination has lifted total cost-of-warehousing for buyers and providers alike, and there is no current signal that it returns to old levels.

The technology cost has moved in the opposite direction, but only for operators who can afford the upfront investment. Warehouse Management Systems (WMS), automation, robotics-as-a-service, augmented-reality-assisted picking and analytics platforms now exist at scales smaller operators could not have accessed five years ago. The benefits (lower error rates, higher picks per hour, better stock accuracy) are real but require a working capital commitment that puts them out of reach for businesses running modest volumes.

The combined effect is that the gap between good warehousing and great warehousing is now bigger than it used to be. A buyer running a traditional, low-tech operation is more disadvantaged today versus a specialist than they would have been ten years ago. That asymmetry is the strongest current argument for outsourcing for businesses where warehousing is not a strategic core.

Rhys Champken

Supply Chain Manager at Lounge

Chain Reaction Podcasts

Supply Chain Runs on Trust First

A trained lawyer turned supply chain manager at one of the UK's fastest-growing fashion brands. Rhys explains why trust — not contracts — holds logistics together.

Warehousing as an asset, or as a liability

The other classic argument for ownership is that warehousing creates an asset on the balance sheet. The land and the building hold value, and that value tends to appreciate over time. This was sound logic when the bulk of a warehouse's economic value sat in the real estate.

The mix has shifted. The value increasingly sits in the technology layer, in the WMS configuration, in the integration between WMS and ERP and TMS, in the data the warehouse generates, in the operational learnings encoded in standard operating procedures. None of that lives on the balance sheet. None of it appreciates passively. All of it depreciates fast if it is not maintained.

A buyer owning a long-leased warehouse building from a 2015 fit-out is, in 2025, holding an asset that is increasingly disconnected from the technology that gives warehousing its current operational value. The real-estate book value may have held up, but the productivity gap versus a 2024 build with current automation can be material. Whether that gap matters depends on how observable warehouse performance is to the customer. For most B2C operators in particular, it matters a great deal.

The follow-on point is about the largest specialist operators. UPS, DHL, GXO, Wincanton and others run multi-year technology investment programmes that an individual mid-market buyer cannot match. Outsourcing into one of those networks gives the buyer access to that investment as an operating expense rather than a capital expense. For businesses that want the productivity without the capital lock-up, the maths now favours outsourcing more clearly than it did a decade ago. The provider-side view of how this dynamic plays out is the subject of our piece on new ways for warehouses to acquire customers.

Control, flexibility and the trade-offs that matter

The strongest argument left for in-house warehousing is operational control. The buyer owns the data, owns the people, owns the decisions. There is no third party between the supply chain leader and the loading bay. For some businesses (those with sensitive product, complex bespoke handling, or operations that diverge sharply from market-standard practice) that level of control has real value.

The counter-argument has matured. Modern WMS platforms exposed to the buyer in real time, RFID and IoT-enabled stock visibility, and contractual data-sharing protocols mean that a well-run outsourced relationship now gives the buyer more granular visibility than most in-house operations achieve. The "I want control" argument is increasingly an argument for better data-sharing, not for in-house operations. We covered the operating discipline behind making that work in how to get the most value from a 3PL.

The flexibility argument is more decisive. Owning warehouse capacity ties working capital to a fixed amount of space at a fixed location. Outsourcing, in particular through on-demand warehousing models, allows the buyer to scale space up and down with the seasonal calendar and to test new geographies without a long property commitment. We wrote about how this plays out in practice in our pieces on finding the perfect UK warehouse location and perfect warehouse rental near you.

For a buyer whose volumes are predictable, stable and unlikely to grow rapidly, the fixed-cost ownership model can still work. For everyone else, flexibility has become a structural advantage that ownership cannot match.

When marketplace plus orchestration changes the question

The cleanest framing of the invest-or-outsource question used to be a binary. Either build your own, or hire one 3PL to do everything. The newer pattern is buyers running a wider set of warehouse partners through a single marketplace plus orchestration layer, which dissolves the binary into a more flexible operating model.

The marketplace layer makes capacity at multiple warehouse providers visible and procurable on commercial terms that do not require a long-term master service agreement with any one of them. The orchestration layer sits above the providers and runs the day-to-day execution: stock allocation across sites, exception management when something fails, visibility of the inventory wherever it sits and the financial flows that settle correctly across multiple providers. The buyer keeps the data, the control and the decision rights. The buyer does not keep the capital tied up in a single building.

This is the operating model FLOX is built around. For the invest-or-outsource question specifically, it changes the answer in two ways. First, it removes the cost of switching, so a buyer is no longer locked into one outsourcing relationship by the difficulty of finding a replacement. Second, it removes the binary itself. A buyer can run a partial in-house operation for core volumes and use marketplace capacity for the flex layer above, with the orchestration handling the integration. The choice between owning and outsourcing was always a stark one because the tooling forced it to be. With a marketplace plus orchestration platform underneath, the choice becomes a portfolio decision rather than a binary one.

For most mid-market and growth-stage businesses asking the invest-or-outsource question in 2025, the honest answer is that the question itself is now somewhat out of date. The better question is what mix of owned, contracted and on-demand capacity fits the business, and what operating layer holds it together.

Subscribe to our newsletter.

Stay up to date with practical insights and useful logistics content

FAQs

Test against two questions. Is warehousing performance directly observable to your end customer in a way that drives buying decisions? And will you invest enough capital to run a top-decile operation if you build in-house? If the answer to both is yes, the case for ownership is real. If either answer is no, outsourcing usually wins on cost, technology and flexibility. For most mid-market buyers in 2025, the honest answer is no on at least one of the two, which tilts the decision toward an outsourced or hybrid model.